SMM August 31, 2025:

Primary Aluminum Alloy: Off-Season PMI Shines Bright as Peak Season Nears, Operating Rate Recovery Hits Bottleneck

The primary aluminum alloy PMI recorded 59.4% in August, maintaining robust performance above the 50 mark despite the traditional July-August off-season. Breakdowns show the production index (70.2%) and new orders index (65.4%) remained elevated, aligning with the overall recovery trend in the sector’s operating rate. While capacity fluctuations in primary processing segments like aluminum billet remained unstable, primary aluminum alloy production continued to gain traction, with orders—particularly downstream finished product exports—performing notably well, reflecting relative strength in both production and order performance. The product inventory index (53.0%) and purchasing volume index (68.5%) indicated stable inventory management and active raw material procurement. The new export orders index (65.4%) remained solid, though external demand uncertainties persist, requiring ongoing monitoring of factors like U.S.-China tariffs.

On operating rates, China’s primary aluminum alloy sector posted a preliminary August rate of 53.8%, up 0.8% MoM and 1.5% YoY. Weekly data showed the rate rose 1.0 percentage point WoW to 55.6% in the first week, followed by another 1.0-point WoW increase to 56.6% in the second week, continuing the recovery trend since July. Against a backdrop of sharp production declines in primary aluminum processing segments like billet and rod, the primary alloy segment shouldered part of the liquid aluminum alloying burden. However, the third week saw the rate flat at 56.6%, while the fourth week dipped 0.2% WoW to 56.4%, signaling a stalled upward momentum.

As September approaches, full production resumptions in primary processing segments like billet have reduced primary aluminum alloy’s role in liquid aluminum absorption. Although tariff war uncertainties have eased this year, and downstream producers’ tentative restocking for the September-October peak season has driven short-term order rebounds, incremental demand remains concentrated among large-scale firms with stable orders, while small and medium-sized enterprises still face weak end-use demand constraints.

Outlook-wise, despite August’s standout PMI and SMM’s positive September PMI forecast, challenges persist from sluggish domestic demand, trade policy uncertainties, and potential high aluminum price impacts. Whether the sector can sustain its strong performance depends on actual demand recovery during the traditional peak season and external factor developments, though overall prospects remain promising.

Aluminum Wheel Exports: Resilient Performance with Volume Growth and Stable Prices. Overseas Peak Season and Trade Landscape Show Improvement.

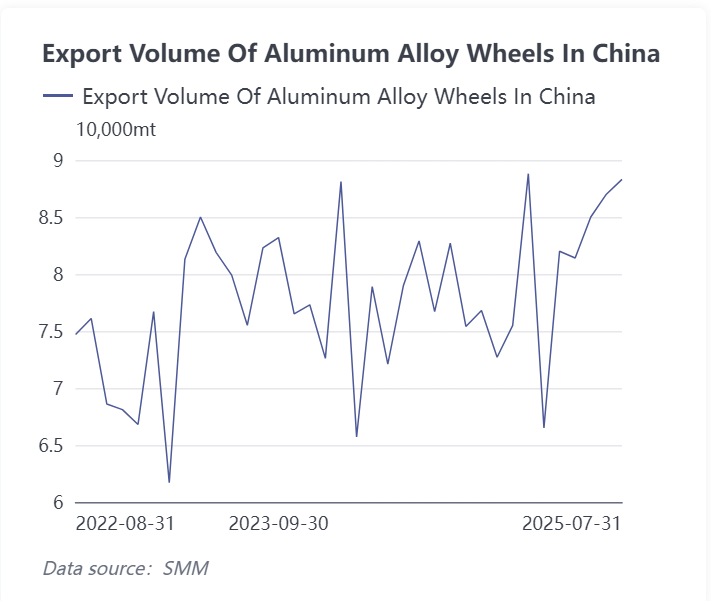

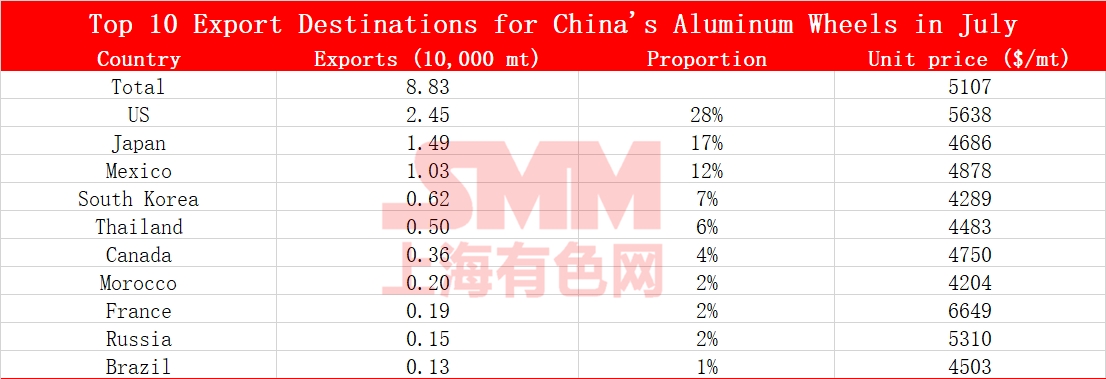

Export data indicates that China's aluminum wheel exports continued their upward trend in August, based on the TOP10 export destinations for June and July, as well as the export volume trend chart for aluminum alloy wheel hubs. The export volume of aluminum alloy wheel hubs rose from 87,000 mt in June to 88,300 mt in July, up 1.5% MoM and 15.2% YoY. After four consecutive months of growth, the figure approached the year's high, demonstrating strong export resilience.

By market, the US market remained relatively stable in aluminum wheel exports despite tariff policy impacts, though attention is needed on price fluctuations affecting profitability. Mexico, as a key re-export hub, maintained its solid market position. Exports to Japan, Canada, and Thailand remained stable in both volume and share, while emerging markets like Morocco and Russia showed growth potential, reflecting the industry's structural adjustments to reduce reliance on single markets.

Looking ahead, as the uncertainty surrounding China-US tariffs diminishes, the overall weak and stable pattern in the primary aluminum alloy and aluminum wheel hub industries is expected to reverse in H2 2025, with aluminum wheel exports likely to maintain their upward trend following the peak season overseas. The primary aluminum alloy sector needs to monitor the actual demand recovery after the traditional peak season in September, while a substantial recovery in aluminum wheel exports will depend on clearer trade policies and effective alleviation of cost pressure.